Times of rapid technological change make poor climates for major waves of new regulation. Consider the Telecom Act of 1996, the first major revision of U.S. telecom law since 1934. The whole point of the act was to open up competition for voice services.

As all now know, that was just a few years before the absolute peak of usage of voice services, and the beginning of the internet era.

As the old adage goes, generals always prepare to fight the last war. That is a useful historical reminder as competition, innovation and business models in telecom prepare to enter the next big era of change.

Our past understandings of how value is created, by whom, and what all that means for business models and competitor fortunes, are about to face historic change. Consider only the fact that unprecedented and huge amounts of new mobile and wireless spectrum are going to be released to support services in the 5G era, dwarfing all existing capacity.

Over the next few years, new spectrum allocations will add more capacity than presently is available for all mobile and Wi-Fi use, by at least an order of magnitude (10 times). Combined with new architectures (small cell), the net increase in capacity might be two orders of magnitude (100 times).

Beyond that, "who" the important providers are might also change. Not only are the two largest U.S. cable TV companies entering the business, but the shift of value towards application, device and platform providers might also mean such firms might become leading providers of mobile and wireless service in the future.

The point is that it is perilous to regulate what might happen in the future when multiple markets now are reforming, blurring the lines between "telecom service providers," application providers, device suppliers and platform companies, all of whom now are taking on new roles.

source: World Economic Forum

The Federal Communications Commission has published proposed auction rules for 24-GHz and 28-GHz spectrum intended to support mobile service. The auctions will represent an additional 1550 MHz of spectrum, more than presently allocated for all mobile operations in the United States, by a wide margin.

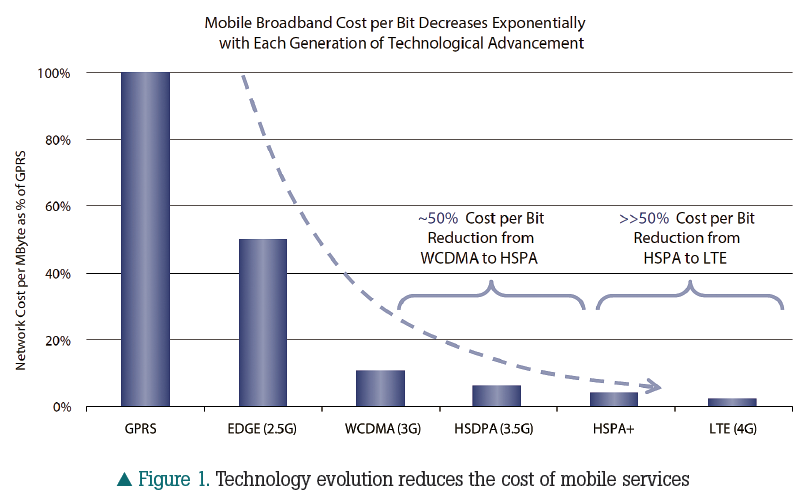

Among other implications, the new spectrum means the cost of acquiring spectrum, on a cost-per-MegaHertz basis, is going to fall. That also means the retail cost of using spectrum, on a cost-per-bit basis, is also going to fall.

In principle, those cost reductions also mean the value of spectrum licenses will fall, on a cost-per-MegaHertz basis.

Such cost reductions are necessary if mobile operators are to challenge fixed network services and become full product substitutes for fixed network internet access.

At the same time, all the new spectrum--especially when deployed to support 5G networks--is likely to erode the commercial possibility of “paid prioritization,” the possible offering of quality-assured consumer internet access.

The reason is simply that 5G services will have latency so low, and bandwidth so high, that the value of any “for fee” quality-assured access is going to be nearly zero.

A cynic might well conclude that most of the frenzied concern about network neutrality is political posturing. As was the case with the Telecommunications Act of 1996, policy advocates are essentially living in the past.

In the 5G era, it will be virtually impossible to argue that a quality of service tier of consumer internet access has much value, since the standard offers will be so much better than anything yet seen on mobile networks.

The same sorts of performance improvements on fixed networks likewise will erode the potential value of paid prioritization, in the consumer services realm.

Business services, as in the past, are not covered by network neutrality rules in any case, so enterprise services can take different paths. Still, the consumer grade 5G services will be difficult, if not impossible, to improve upon.

It is the universal vision that 5G, with a move to edge computing, is going to reduce application latency in ways that likewise make paid prioritization a non-viable commercial possibility.

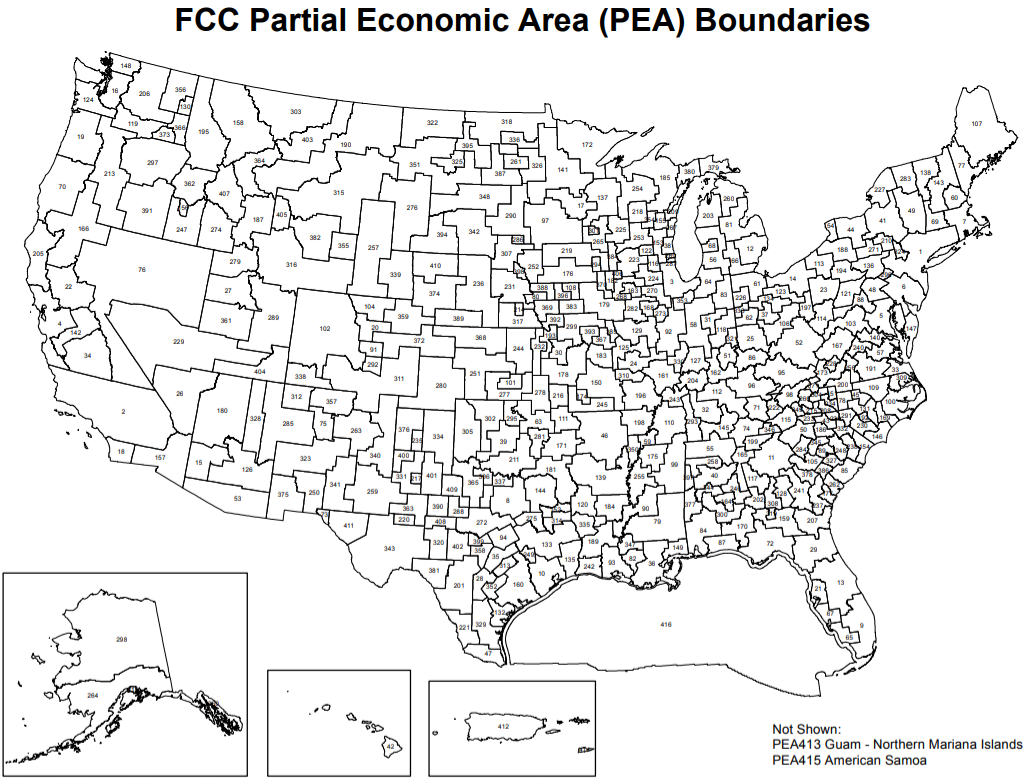

In the 28 GHz band, the Federal Communications Commission plans to auction 425-MHz blocks of spectrum. In the 24-GHz band, licenses will be for 100-MHz blocks of spectrum.

The 28-GHz licenses will be auctioned by county, and two licenses per county will be available. That auction potentially will place 850 MHz of new spectrum into commercial use, on a nationwide basis (850 MHz in every area).

The 24-GHz licenses will be by partial economic areas, which amalgamate numerous counties. Seven licenses will be available in each 24-GHz PEA. That auction potentially will add 700 MHz of additional mobile spectrum in commercial service, on a national basis (700 MHz in each area).

new millimeter wave spectrum