Singapore is among few internet access markets where a statement such as “the jump from 500 Mbps to 1 Gbps really is not that great” actually can be made. In most fixed internet access markets, and for most potential customers, the option is not yet available.

That noted, in markets where gigabit internet access is widely available, the pricing premium for a gigabit service--compared to a 500-Mbps service--ranges from between 16 percent to 40 percent, according to Ovum.

On the other hand, at the moment, it appears that a boost to 10 Gbps offers “much greater revenue growth potential,” according to Ovum analyst Kamalini Ganguly. Optimists might well argue this is the case as faster speeds have in the past provided a rationale for higher prices, and a doubling of speed from 500 Mbps to 1 Gbps will be dwarfed by a boost of an order of magnitude (10 times) from 1 Gbps to 10 Gbps.

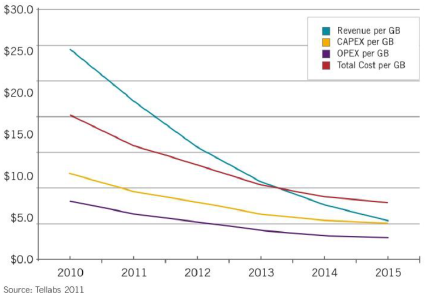

It would be historically correct to note that, over time, the cost per delivered gigabit of data has declined. It also would be true to note that, over time, customers consume more data. So lower units costs are balanced by higher consumption.

That is largely the reason why average revenue per account for mobile data tends to grow, over time. The only issue is how wide the revenue delta will be as speeds continue to rise, and end user consumption continues to rise.

By one line of reasoning, end user willingness to pay cannot exceed growth of disposable income, household income or a certain percentage of total household income, absent other key changes in spending habits.

In other words, if typical spending is two percent to three percent for all communications services, mobile services or data services, most buyers are unlikely to change those patterns very much, over the long term. To change the consumption curve in a significant way, spending on other products has to decrease, or household income has to increase (the rising tide that lifts all boats, even if spending percentages do not change).

Also, much hinges on the degree of competition and adoption rates, one rightly might argue. That already has been the case. If past is prologue, the revenue boost from 10 Gbps might not be as great as some hope.

So far, gigabit services have boosted internet service provider revenue only up to 11 percent, says Ovum. “Reasons for that include low premiums in competitive markets and lack of take-up of gigabit services.” In other words, low adoption rates and competitive pricing have limited the ability to sell the higher-priced services.

Ovum bases its conclusions, apparently in part, on present experience of 10-Gbps services.

“The lowest 10-Gbps price premium we found was 47 percent,” said Ovum. That was the posted retail tariff for Singapore ISP M1's premium over its own 5-Gbps plan.

“The premium increases to 173 percent if compared with the 2-Gbps services. In other markets, the 10-Gbps premium over 1-Gbps ranges from 215 percent to 327 percent,” Ovum says.

Several caveats likely are in order. Historically, though price premiums for faster-speed services, as with mobile internet plans featuring higher usage, have cost more, such price premiums tend not to last.

Among the reasons: over time, the leading offer becomes a standard offer, with standard pricing; customers tend to upgrade, but not to the highest level of service; so over time, the standard offer is deemed “good enough” by most consumers.

That might not be the case for enterprise and business buyers, who logically are the lead buyers for the fastest services.

“The higher price points mean that 10-Gbps services are aimed more at enterprises (which have higher and symmetrical bandwidth requirements) and within the consumer segment at subsegments such as high-end gamers, who can afford the higher price points,” Ovum argues. “Other target groups include SMEs with large content requirements.”

The point is that there are some reasons to predict growing spending by accounts on internet access services, based on growing consumption and faster speeds. Just how much spending can grow will be bounded by growth of household income, shifts in consumption patterns, the degree of competition in each market and advances in technology.

But some of us will argue that it is the limitation of disposable income that will be key. There is only so much a typical household or person will spend on internet access. That is less the case for business accounts, but even there, a limit remains as to how much total communication spending will happen. That also tends to be a function of entity income (revenue and earnings).