One often-cited bit of advice for mobile operators trying to change their value propositions is to wrap more functionality around their core offers. That does not mean "moving up the stack" (occupying new positions in the ecosystem) so much as enhancing existing offers.

Sometimes mobile operators do want to move into different roles within the ecosystem, though. A common bit of advice is to partner to accomplish such objectives. Such deals can be low-margin gambits, though.

For starters, profit margins typically are difficult, because there is a cost of goods issue, especially for services that already have low profit margins.

Any business deal requires that all parties gain value from any transaction. So when any service provider wants to partner with another application provider, value has to exist for both parties.

You might argue that one reason tier-one service providers have not have much success partnering with voice or messaging application providers, to compete with independent providers of over-the-top voice and messaging apps, is that too little value generally exists for the potential app partner.

That is the logical consequence of the way we have decided to build the next-generation telecom network. Those of you with long memories will recall a number of such attempts.

One might argue early business data networks such as X.25 or frame relay were not intended to be universal solutions. But efforts to build general purpose next generation networks have been numerous.

Some will recall ISDN (integrated services digital network) and its successor, “broadband ISDN” (later known as ATM, or asynchronous transfer mode. Some of you also will recall the huge debates about whether sticking with ATM made sense, or whether the industry should shift to Internet Protocol.

Those debates were hot and heavy two decades ago, when many now in the industry were not born, or were youngsters. ATM lost and IP won, in large part for cost reasons. Ethernet connections were widely deemed to be ubiquitous and well down the cos curve, compared to ATM customer premises equipment.

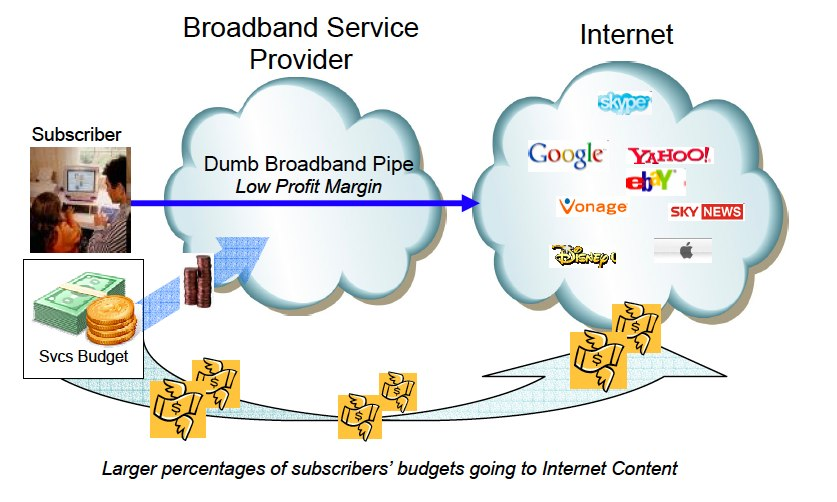

There are some important consequences. Once IP becomes the next generation protocol, all applications essentially become “over the top” apps, no matter who owns the apps. That is worth emphasizing.

In an IP environment, no application provider “needs” a business relationship with an access provider. That, in turn, affects all potential partnerships between access providers and app providers.

Simply put, application providers need no business relationships with access providers to get access to their potential users and customers. Service providers, on the other hand, tend to be the entities that “need” partnerships.

Every successful business deal requires an exchange of value for all parties. In an IP environment, app providers do not “need” such relationships with access providers to reach their customers. That limits the value any access provider brings to any potential deal.

source: ZDnet