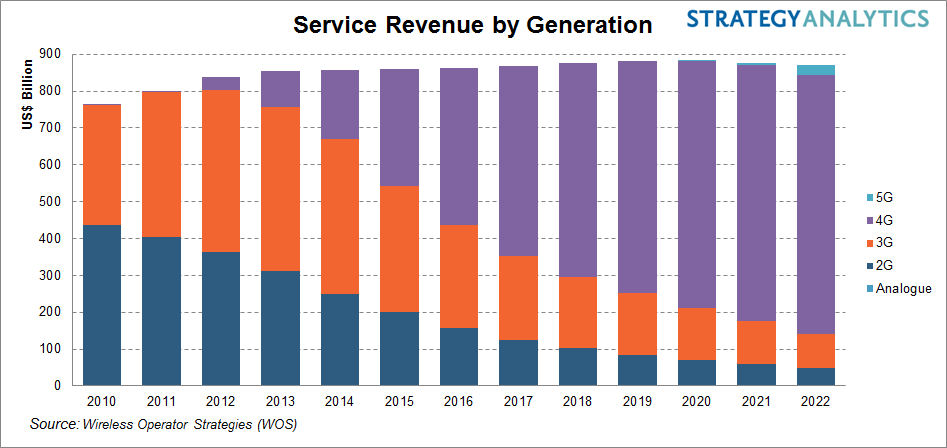

The conventional wisdom is that 5G is going to create new revenue sources for mobile operators. That undoubtedly will prove true, to an extent; and perhaps to a significant extent.

What remains unclear is whether 5G actually will produce a net increase in mobile broadband revenues, even if 5G produces a gross increase in such revenues.

In other words, on a net basis, it is conceivable that 5G literally produces no net gain in access revenue. The reason is that, unlike the case in the 3G era, the 5G mobile internet market is going to operate in a mature environment in most markets.

In the transition from 2G to 3G, one might note an overall increase in mobile operator revenues, as the internet access market was young. By the time 4G arrives, growth mainly is substitution, not net growth. That is likely to be the case in the 5G era as well.

To wit, new 5G revenues will include some element of actual growth (IoT subscriptions, for example). But many of the 5G accounts will simply be substitutes for existing 4G subscriptions, so there will be no net gain in subscriptions.

Some will hope for higher average revenue per account. Initially, that could happen. But ARPU will fall fast. So, on a net basis, it is possible there will be no actual gain in mobile data or total mobile revenue.

Some might well ask, “then why do it?” The simple answer is that “doing nothing” might plausibly result in serious negative revenue growth, which is worse than “flat revenue.”