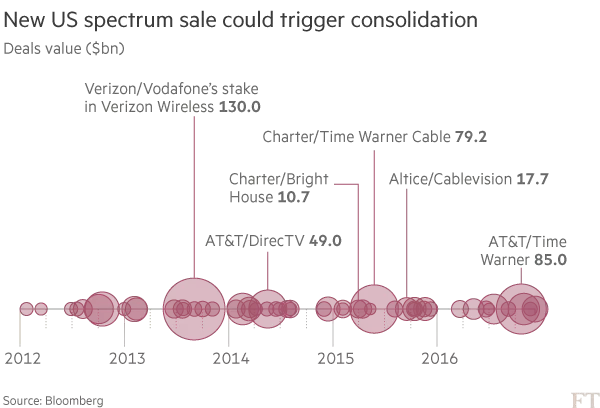

Virtually everyone expects a serious round of U.S. industry consolidation, in 2017, in the mobile, content and content distribution markets. Sprint, T-Mobile US and Dish Network are among firms usually mentioned as potential actors (either as buyers or sellers). Comcast, Altice and Charter Communications also often as seen as potential players.

Up to this point, most industry mergers have been of the “horizontal” variety, intended to provide additional scale. But that strategy has nearly run its course. At some point, antitrust concerns prevent further scale of that sort.

There is an equally-important consideration.

Some would argue the more-important mergers are of the vertical variety that move access providers up the value stack into content, applications, transactions or advertising. Scale helps with costs and gross revenue.

But scale does not help a participant escape a lower-value role in the ecosystem.

Other than Comcast, only AT&T has made major moves in that regard. So the next round might well be focused on vertical combinations, the salient possible exception being a horizontal merger between Sprint and T-Mobile US.

Even a move by cable TV operators into mobile facilities ownership is more a vertical diversification move (expanding business operations into different steps of a single ecosystem) than a scale move designed to increase mass in an existing business category.

There are many reasons for that likely outcome. First, there normally are limits to the amount of market share allowable in any horizontal combination that makes any provider a bigger market share presence in a specific industry segment (mobile, fixed access, cable TV). The broad rule of thumb has been that no single provider in the fixed segment is allowed to serve more than about a third of total U.S. homes.

The other angle is that virtually all would-be market leaders coming out of the access or content distribution business know they have to acquire bigger profiles in the higher-value, more-sustainable content production, applications and services portions of the ecosystems.

In that regard, a move by a fixed network provider into the mobile segment is not a scale move (more of the same), but a vertical move into a new part of the ecosystem.