I was chatting with a banker recently about the use of mobile phone behavior to assess borrower risk in areas where most people do not have credit scores or banking relationships. She was skeptical. I don’t blame her.

But many now believe that analysis of mobile data relationships, communities, frequency of communication and other evidence based on mobile phone use could, indeed, be used to assess credit risk.

There are many straightforward indicators of behavior that are plausibly related to loan repayment. A responsible borrower may keep their phone topped up to a minimum threshold so they have credit in case of emergency, whereas one prone to default may allow it to run out and depend on others to call them.

An individual whose calls to others are returned may have stronger social connections that allow them to better follow through on entrepreneurial opportunities.

As you would guess, such techniques are most valuable in the global South.

One obvious source of data is remittances received on a phone (M-Pesa, for example). It seems to make a difference whether contacts on a mobile phone include both first and last names, for example.

That bit of data can mean a 16-fold difference in default rates on loans. Micro-loan provider Tala analyzes mobile phone behavior such as the size of the applicant’s network. Consistency, like making a daily call to parents, and where a person goes daily make a difference.

About eight to 10 questions seem to be enough to establish a proxy creditworthiness score.

Certain behavioral patterns are remarkably accurate in predicting the probability of default among borrowers without formal financial histories, even for very poor borrowers whose mobile phone usage is extremely limited, according to studies cited by the World Bank.

Higher-risk borrowers used their phones infrequently, and were found to only place 22 minutes of calls and send one text messages, spending a total of $2.85 over a period of 11 weeks.

Individuals in the highest quartile of risk were six times more likely to default than those in the lowest quartile.

A bank that participated in a study found it could eliminate 43 percent of loan defaults by eliminating the 25 percent of people who are most risky.

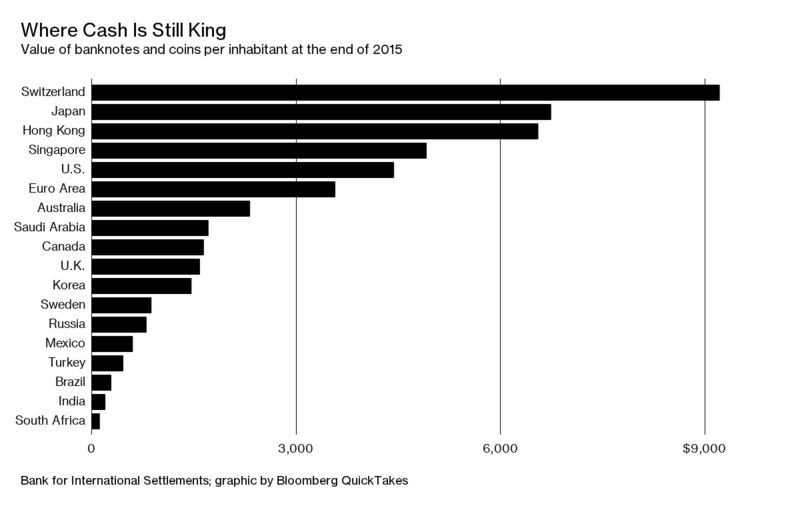

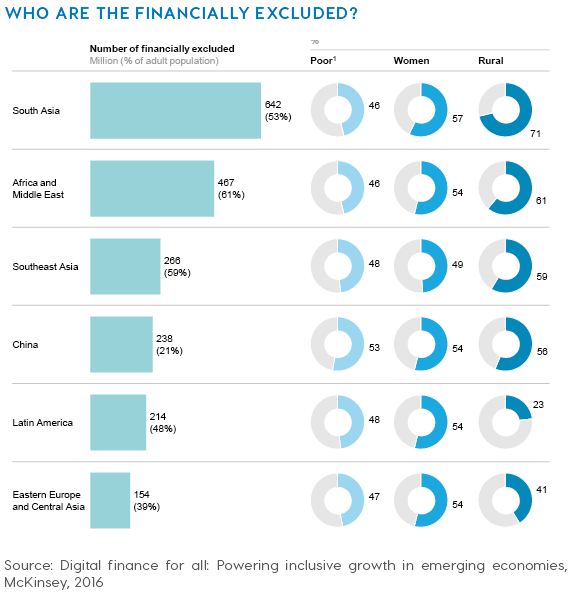

At one level, this chart only illustrates the fact that developed nation citizens have more income, cash or wealth than citizens in developing nations.

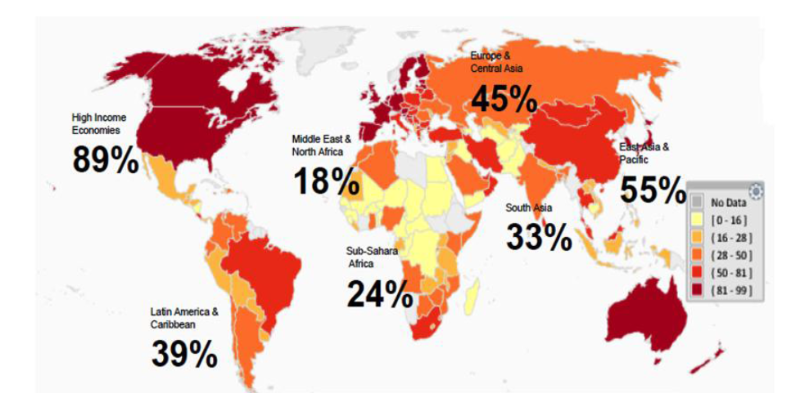

Likewise for digital payments, citizens in developed markets tend to use such mechanisms more than citizens in developing nations.

No comments:

Post a Comment