Unlimited mobile internet plans, whatever qualifications are placed on use of those plans, strike at the heart of hopes to monetize increased mobile internet usage. That is a huge tactical problem, even if--strategically--”everyone” has known for some time that significant future revenue growth could not be driven by consumers using smartphones or other devices.

Price wars do not help. Nor does ability to monetize higher usage by levying higher per-unit (consumption-based) prices. “Nobody” would seriously propose that consumption of fresh drinking water, electricity, heating fuels, groceries and other consumer goods be charged on an “all you can eat” (unlimited) basis.

Supply and demand clearly matter. The scarce asset, for any communications network supplying “access” now is internet usage (gigabytes instead of voice minutes of use).

For a “best effort” service, contention and network loading therefore become key issues.

For a “best effort” service, contention and network loading therefore become key issues.

Ironically, as consumers have chosen to consume less voice, less text messaging, less long distance calling, network load has lessened enough, for such low-bandwidth apps, to allow “unlimited consumption of products nobody wants to use much of.”

The problem Verizon, AT&T and others clearly face is that if unlimited-usage plans remain in effect, and if they become the “dominant” plans consumers purchase, then higher usage cannot be monetized directly.

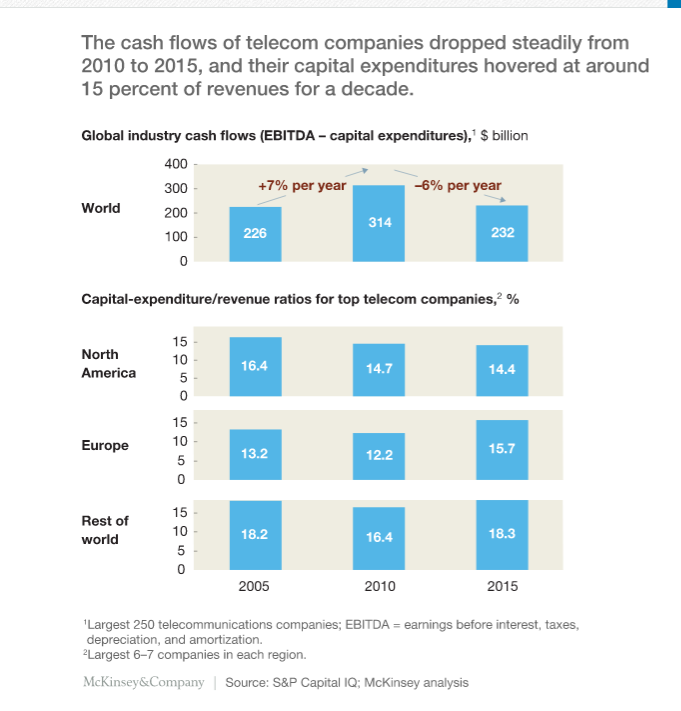

That comes against a backdrop of “slow to no growth” globally.

Mobile operator revenue and cash flows at the largest 250 global companies have dropped by an average of six percent a year since 2010, according to McKinsey analysts.

From 2010 to 2014, the telecom business entered a period of slow decline, with revenue growth down from 4.5 percent to 4 percent, EBITDA margins down from 25 percent to 17 percent, and cash-flow margins down from 15.6 percent to eight percent.

Among US telecom companies, for instance, landline and mobile voice now account for less than a third of total access, down from 55 percent in 2010, while data revenue has risen from 25 percent of total revenues in 2010 to 65 percent today.

It likely is worth noting that the greatest driver of consumer internet bandwidth is video. If usage cannot be monetized directly, it will make sense to try and monetize in other ways, such as owning the video service assets consumers pay for, video assets that can be monetized by advertising, or other apps for which consumers will pay an additional fee.

No comments:

Post a Comment