Assumptions always matter when conducting studies. But assumptions also are important when looking at levels of capital investment at aggregate levels. Firm priorities can vary. Industry segment patterns can be quite distinct. Also, "capex" includes all manner of investments not directly related to network investment.

It is worth noting that “capex” includes lots of spending (trucks, customer premises equipment, international spending, smartphone leasing, buildings and computing gear) that might not contribute to our assessment of “network” investment.

Also, big mergers and acquisitions, plus spending on customer premises equipment, can skew reported capex. When total spending is deemed to have changed in low single digits, such nuances can make the difference between growth or decline, on a reported basis.

The crucial question is what would have capex been if Title II had not been imposed, controlling for other factors.

It is worth noting that “capex” includes lots of spending (trucks, customer premises equipment, international spending, smartphone leasing, buildings and computing gear) that might not contribute to our assessment of “network” investment.

Also, big mergers and acquisitions, plus spending on customer premises equipment, can skew reported capex. When total spending is deemed to have changed in low single digits, such nuances can make the difference between growth or decline, on a reported basis.

USTelecom’s seventh annual report on U.S. broadband investment numbers is not available yet, but “our initial analysis strongly suggests that investment in 2016 continued to trend downward following the Federal Communications Commission’s (FCC) adoption of the 2015 Open Internet Order,” says Patrick Brogan, UST VP.

Data compiled from internet service providers representing 90 percent to 95 percent of annual industry capital expenditures, suggests the dip in broadband investment UST reported on in 2015 was not a one-off occurrence.

In 2016, capital expenditures was $71 billion, down from $73 billion in 2015 and $74 billion in 2014, UST says, an amount $2.5 billion to $3 billion lower in 2016 than it was in 2014, the year before the FCC adopted Title II utility regulations.

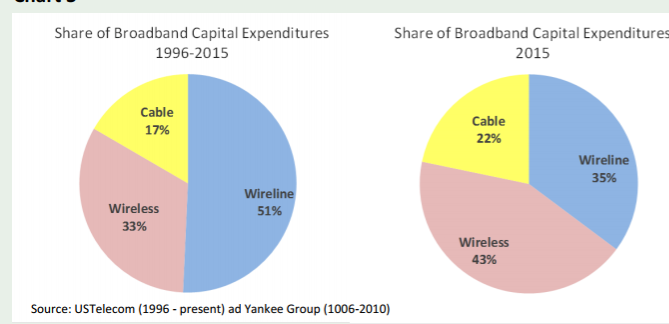

The amount of U.S. capital investment is highly contested. Clearly, cable TV operator capex was up; fixed network capex was down and mobile capex was up, though one has to adjust for the impact of handset subsidy accounting rules. Financing of smartphone handsets is “capex” under accounting rules, but does not help us understand changes in network capex.

That noted, some studies suggest higher capex under common carrier rules, while others argue the opposite case.

Claims by some that broadband provider capex increased in 2015 and 2016 ignore accounting adjustments for certain non-material items like leased cellphones and acquisitions, such as AT&T’s merger with DirecTV and a Mexican wireless operation, UST argues.

The crucial question is what would have capex been if Title II had not been imposed, controlling for other factors.

No comments:

Post a Comment