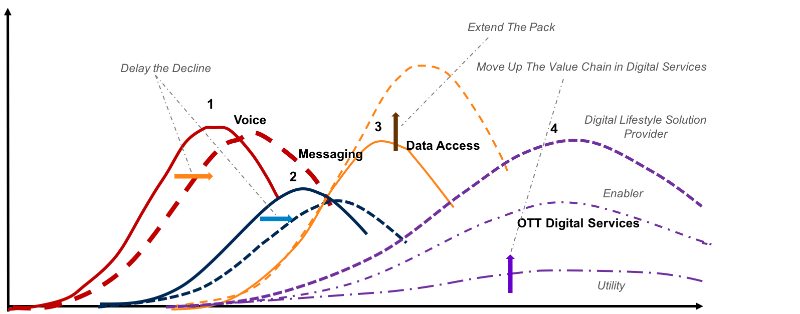

Every legacy retail access service supplied by cable TV and “telco” providers in most developed markets arguably has passed its product cycle “peak.”

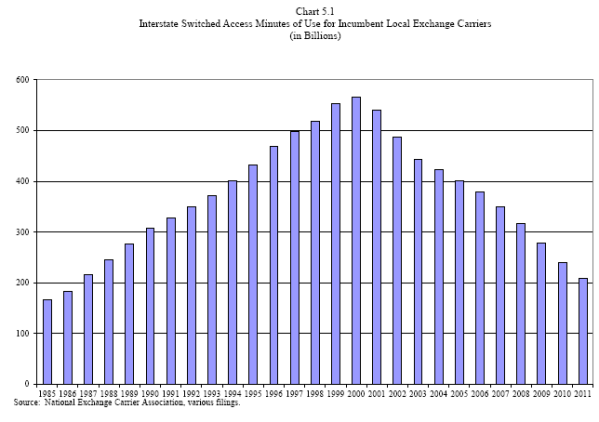

U.S. voice lines peaked in 2000 or 2001, for example, as did long distance minutes of use. Text messaging revenues also are falling. Fixed network internet access markets are reaching saturation as well (in terms of accounts). The degree to which mobility services will limit further growth, and then possibly cause fixed network internet access decline is among the next big issues.

The offsetting trend is data access to support internet of things apps and services, which will add accounts and revenue, though not with the same level of average revenue per account. On a per-device basis, IoT devices might represent monthly revenue an order of magnitude lower than services for smartphones, for example.

Still, demand for internet access connections “for humans” is reaching saturation, in either fixed or mobile realms. That trend remains latent in many emerging markets, where net growth of accounts and revenue is possible.

Eventually, though, even burgeoning mobile adoption and mobile internet access in emerging markets likewise will peak.

That is why internet of things is considered so strategic a development in the access business: it represents the single biggest new revenue driver to replace lost legacy revenues over the medium term.

At the same time, value and revenue within the communications and internet ecosystem are shifting to the application layer. That, in a nutshell, explains the key strategic problem for every tier-one access services provider, and the danger for small access providers.

Over time, tier-one providers must become significant owners of new application assets that are used by digital appliances and delivered over access networks. That will be the case even if IoT develops robustly as a new market for access connections.

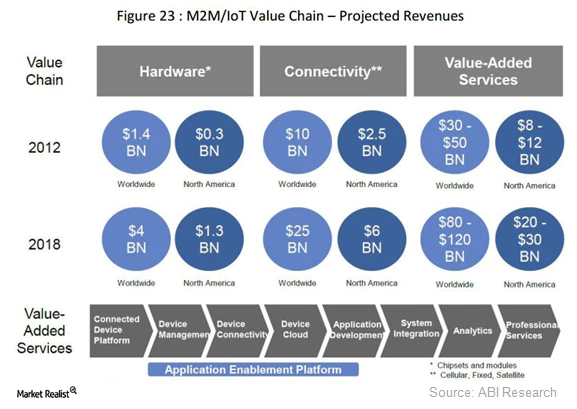

As one forecast by ABI Research suggests, as important a market as internet of things could be, more revenue will earned by app and service providers than by connectivity services (about three to five times more app/service revenue than “connectivity” revenue).

No comments:

Post a Comment