Neither Google nor Facebook are being anything but transparent about their own roles in new parts of the Internet ecosystem, whether that is moves into e-commerce as a foundational business model, pioneering use of new Internet access platforms or accepting new roles in app hosting, transport or backhaul.

Long past is the time when Google or Facebook solely sourced their global connectivity from capacity providers, their networking gear from traditional original equipment manufacturers or their data center requirements from third party data center operators.

Having achieved huge scale, both firms now can make different “make versus buy” decisions. And the increasing trend is to “make” rather than “buy.” That makes the large app providers clear examples of “frenemies.”

They both buy from, and compete with, traditional suppliers of transport, access, data center support, networking gear and software.

In many markets, that should lead to many new opportunities to work with the likes of Google and Facebook as backhaul and transport providers.

That is how Google, Facebook and most proposed low earth orbit satellite constellations are planning on coming to market with new Internet access platforms. Basically, all propose use of their new platforms for backhaul and transport.

That said, Google Fiber and Nexus also directly compete with existing suppliers. In India, both Google and Internet Basics (Facebook) are working with existing Internet service providers to build out public Wi-Fi networks.

And though the decisions will be no easier than in the past, affected contestants will have to decide how to work with, or compete with, the likes of Google and Facebook at many layers of the protocol stack, not just the physical and transport layers.

In most cases, access and transport providers will mostly avoid competing at the application layer. At some point, scale advantages held by the biggest app providers are too great to overcome.

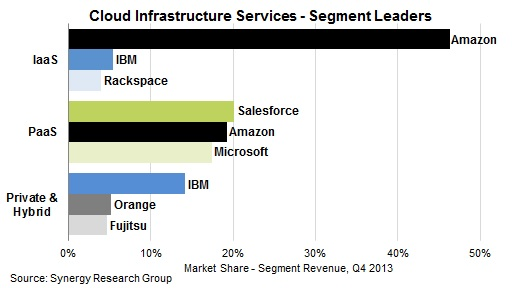

That appears to be a growing reality in the cloud computing business, where public cloud increasingly is concentrated among the ranks of Amazon Web Services, Microsoft and Google, many would argue. Private and hybrid cloud computing continues to be the place where others have significant market share.

Private cloud continues to offer more opportunity for rival suppliers. By 2018, 31 percent of cloud workloads will be in public cloud data centers, up from 22 percent in 2013. That represents a compound annual growth rate (CAGR) of 33 percent from 2013 to 2018.

By 2018, 69 percent of the cloud workloads will be in private cloud data centers, down from 78 percent in 2013. That represents a CAGR of 21 percent from 2013 to 2018, according to Cisco.

The point is that there are few completely fixed roles in the Internet ecosystem. That means every contestant will compete with, and cooperate with, other participants at various times, in different places, for distinct reasons.

Perhaps there are other implications as well. Most observers of business strategy would note that, over the long haul, a bifurcated, or barbell structure tends to develop.

That is to say, there are a relatively few market leaders with most of the share (customers and revenue), but also many many small firms with some niche strategy, dependent for success on the very inability of large firms to compete in small markets.

If so, then there might be many new opportunities for specialists, even in the scale-driven consumer services business. Large providers will continue to dominate the “commodity” parts of the business.

Specialists will have greatest opportunities in niches of various types, geographic or functional. Only a large firm might be able to supply mobile services effectively and sustainably across a subcontinent.

But it also is likely there will be room for local specialists as well, even in the “commodity” Internet access business, simply because the large-firm business model will not work everywhere, always.

No comments:

Post a Comment