On some measures, U.S. consumers have access to, and use, faster Internet access services, more than consumers in Europe, in large part because U.S. policies have encouraged investment, compared to European policies that historically have been more focused on wholesale access to encourage competition.

It also would be fair to note that most communities have access to at least two facilities-based providers, a fact that arguably has encouraged investment in upgraded facilities.

Google Fiber’s entry also has had a direct impact, encouraging other Internet service providers to drop their prices to $70 to $80 a month for gigabit access, and to invest in such facilities.

Some would argue Google Fiber’s decision not to allow wholesale access, and thus reap the benefits of capital and operating investments, is one example of how there are incentives to invest. Google Fiber cannot be compelled to sell wholesale access, especially at low rates, to other competitors.

A far greater percentage of U.S. households have access to Internet access at 25 Mbps or faster, the study argues.

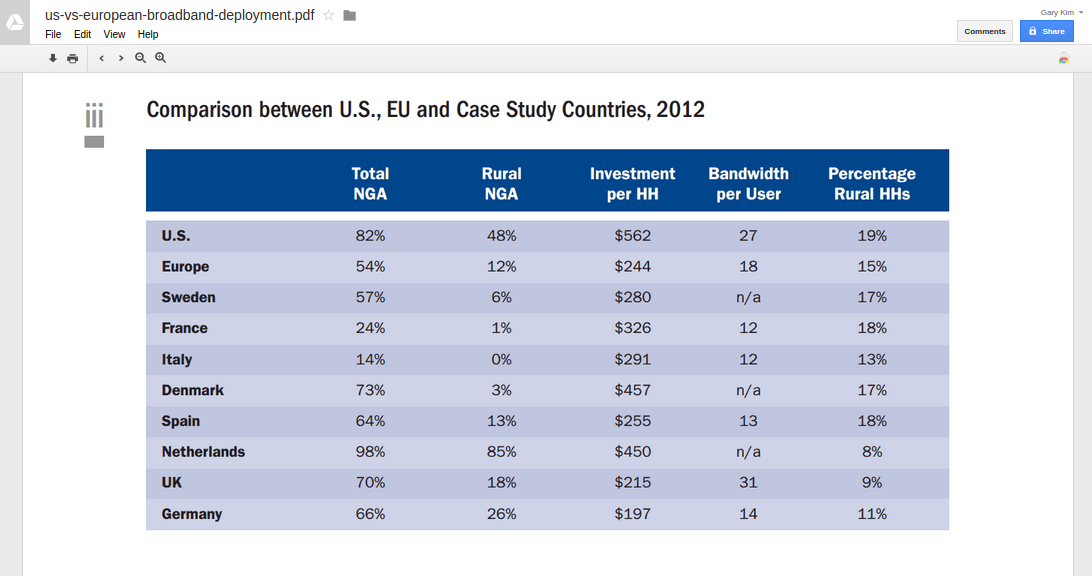

On a national basis, 82 percent of U.S. consumers can buy access at 25 Mbps or faster, compared to 54 percent of Europeans.

In rural areas, 48 percent of U.S. rural consumers have access to 25 Mbps or faster services, compared to 12 percent in Europe, according to a study by Christopher Yoo, University of Pennsylvania law school professor.

The study also found that the United States had 23 percent fiber-to-premises coverage, compared to 12 percent in Europe.

The United States also has 86 percent coverage of Long-Term Evolution (4G LTE), compared to 27 percent LTE coverage in Europe.

U.S. download speeds during peak times (weekday evenings) averaged 15 Mbps, below the European average of 19 Mbps, however.

During peak hours, U.S. actual download speeds were 96 percent of what was advertised, compared to Europe, where consumers received only 74 percent of advertised download speeds.

U.S. consumer experience in the areas of latency and packet loss also was better than in Europe.

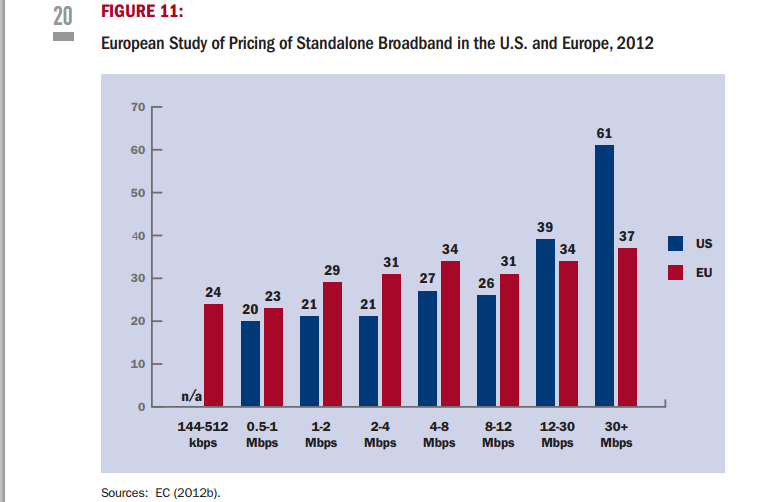

U.S. broadband “stand-alone” prices were cheaper than European broadband for all speed tiers below 12 Mbps.

U.S. broadband was more expensive for higher speed tiers. The caveat is that most U.S. consumers do not appear to pay “stand-alone” prices for fixed network broadband, typically buying bundles that in essence discount prices.

Consider that 97 percent of AT&T customers bundle their video subscription service with other AT&T services. Cable providers have 75 percent or more of their subscribers on a bundle of video and broadband, AT&T notes.

Standard coverage is available in 99.5 percent of U.S. households and 99.4 percent of European households. Standard fixed coverage is available in 95.8 percent of U.S. households and 95.5 percent of European households, the study found.

Mobile broadband coverage at 3G speeds also fall within quite similar ranges, covering

98.5 percent of U.S. households and 96.3 percent of European homes.

Yoo attributes a regulatory “light touch” for higher U.S. investment in broadband and expanded access to high-speed internet in the US compared to Europe.

The University of Pennsylvania Law School study also showed that Europe’s treatment of broadband as a public utility, which some net-neutrality advocates are pushing for in the US, has hindered internet access growth there.

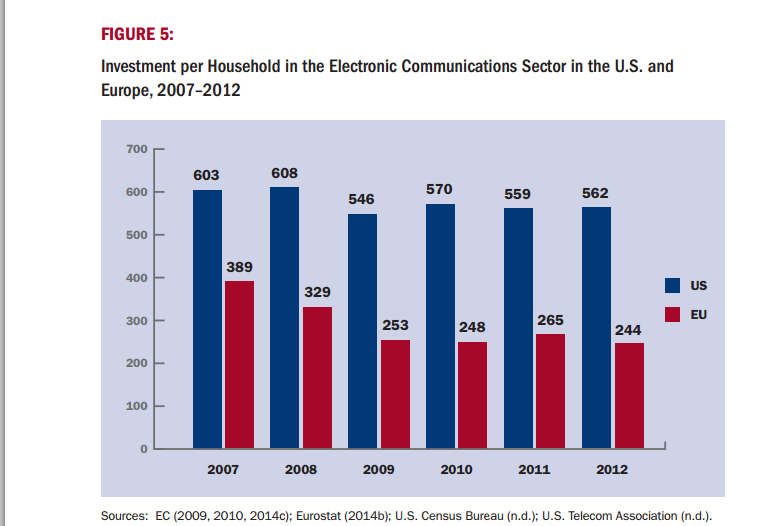

The study notes that, in Europe, where telecom service revenues have fallen by more than 12 per cent since 2008, the financial return for investing in next-generation networks is less promising, since those facilities must be leased to competitors, allowing them to avoid building their own networks.

Those rules also reduce the “scarcity value” of new networks, though.

“The empirical evidence thus confirms that the United States is faring better than Europe in the broadband race and provides a strong endorsement of the regulatory approach taken so far by the US,” said the study, which was written by law professor Christopher Yoo.

The differences in regulatory regimes also contributed to $562 of broadband investment per household in the US versus $244 per household in Europe, where regulators treat broadband as a public utility and promote service-based competition where new players lease existing facilities at wholesale cost.

U.S. policy has emphasized facilities-based competition by firms that can build new facilities, and then reap any rewards, without enabling competitors.

U.S. policy also shows the importance of competition between cable TV and telcos. Although many advocates regard telco fiber to the home as the primary platform for faster networks, the data suggest otherwise.

In Europe, DOCSIS 3 (39 percent coverage as of 2012) and VDSL (25 percent) both contribute more to fast network coverage than does FTTP at 12 percent.

In terms of actual subscriptions, the distribution skews even more heavily towards cable connections (DOCSIS 3), with 57 percent of subscribers, followed by FTTP at 26 percent,

and VDSL at 15 percent.

Even if one were to focus exclusively on FTTP coverage, the data clearly give the edge to the U.S. market. As of the end of 2011, FTTP service was available in 17 percent of U.S.

households and 10 percent of European households. By the end of 2012, FTTP service increased to 23 percent of U.S. households and 12 percent of European households, the study found.

But mobile Internet access now is more important than ever. As of the end of 2011, Long Term Evolution networks covered 68 percent of the U.S. population and eight percent of European households.

By the end of 2012, LTE coverage increased to 86 percent of the U.S. population and 27 percent of European households. Note the difference in data collection, though. European dat is “by household.” U.S. data is by “person.” That understates European coverage figures, to the extent that households have more than a single occupant.

On the other hand, average download speeds at peak periods are higher in Europe, compared to the United States.

No comments:

Post a Comment