Despite the emphasis on creation of “new services” to drive the next waves of revenue growth in the local access business, the actual revenue gains so far have been driven mostly by market share shifts among mobile, fixed network telco, cable TV and satellite TV firms.

That is not to discount share shifts to independent providers of all sorts, including competitive local exchange carriers, independent ISPs and resellers. But most of the measurable volume of U.S. market share change occurs in just two segments: fixed network telco and cable TV.

You know the story: telcos are taking video market share, and ceding voice market share to cable TV. Cable TV companies are losing video share, but have gained voice services share.

Most would say cable companies retain an edge in high-speed Internet access.

In the business customer segment, fixed network telcos have been slowly losing share to cable TV operators, but also blunting inroads of the independent and competitive providers. The exception is a few independent fixed network telcos that have moved agressively into the small business services segment (Windstream and Frontier Communications being the salient examples).

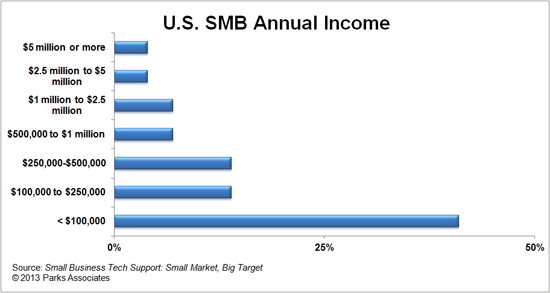

Insight Research Corporation predicts U.S. cable companies in 2013 will reach $8.8 billion in annual revenues providing telecommunications services to small and medium-size businesses.

U.S. fixed network telcos probably have about $6 billion iin video subscription revenues, based on an attribution of video at $50 a month, on a base of about 10.4 million subscribers.

Next to mobility, business services are the second largest segment in the $500 billion U.S. telecommunications business.

According to Insight Research, cable companies already have about 10 percent of the business market for voice and data services. At $8.8 billion, the addressable market is $89 billion annually.

There is huge logic to the cable push. Most tier-one telcos consider small businessto be part of the “mass markets” operation. Given the historic consumer orientation of cable TV companies, selling voice and Internet to small businesses is not a huge shift.

Of course, cable operators also sell to enterprises, especially for high-capacity private networks and mobile backhaul connections.

In the future, cable operators probably also will get a share of the backhaul market for small cells.

The point is that, so far, the "new" revenue streams for cable TV operators and fixed network telcos have come from legacy services, albeit legacy revenues taken from existing providers.

At some point, that trend will run its course and "truly new" services (sensor connections for machine-to-machine or Internet of Things applications), automobile communications, home automation and other revenue sources will have to be created.

For some time to come, market share shifts will continue to drive the significant portion of service provider "new services" growth.

No comments:

Post a Comment