Policy makers and regulators need to ensure enough supply to maintain sufficient backhaul for wireless networks, especially if there is insufficient fixed access network competition, a new report by the Organization for Economic Cooperation and Development says.

Policy makers and regulators need to ensure enough supply to maintain sufficient backhaul for wireless networks, especially if there is insufficient fixed access network competition, a new report by the Organization for Economic Cooperation and Development says.

The challenge for regulators is that, regardless of the technology used, many parts of the OECD look likely to face monopolies or duopolies for fixed networks. Wireless can provide competition, but spectrum availability will always impose limits that are not a constraint for fiber networks.

Fixed networks have, in effect, become the backhaul for mobile and wireless devices with some studies claiming that 80 percent of data used on mobile devices is received using Wi‑Fi connections to fixed networks.

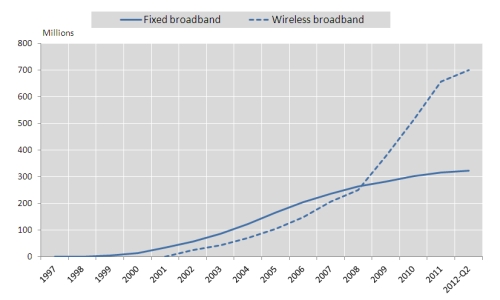

Wireless and fixed broadband subscriptions in OECD countries

Policy makers and regulators have a vital role to play in ensuring sufficient competition, the study argues. This includes making sure there is adequate available spectrum, abundant IP addresses or other numbering resources for new market entry, and fair competition between operators and over the top providers.

Ensuring markets remain open to OTT and facilities‑based providers is essential to innovation in broadband infrastructures, and critical to addressing major industry and broader economic and social challenges.

A growing number of industry leaders claim high prices for international mobile roaming are detrimental to their relationship with their customers, and a significant barrier to trade and travel in OECD economies. The OECD Recommendation of the Council on International Mobile Roaming Services (February 2012) recommends removing such barriers to lower-cost roaming.

Among other findings, the study points out that telephony costs have continued to fall, at least up to the 2012 period for which the OECD report reports results.

In 2011, mobile subscriptions represented 65.4 percent of paths, up from 64 percent in 2009, while use of traditional fixed telephony subscriptions continued to decline.

The average subscription rate of mobile Internet access in OECD countries as a whole rose to 56.6 percent in June 2012, up from just 23.1 percent in 2009.

Prices for fixed telephony and, more markedly, for mobile voice services decreased from 2010 to 2012, showing significant declines across all consumption patterns, with the exception of fixed business services.

A laptop‑based wireless broadband usage bucket (offers within the 500 MB per month range) cost US$13.04 on average across the OECD in purchasing power parity terms, although it reached US$30 in some countries.

Average expenditure was US$37.15 for a 10 GB bucket. A 250 MB tablet package cost US$11.02 per month on average. A 5 GB basket for tablets cost US$24.74 on average, but varied from US$7.98 (Finland) to US$61.84 (New Zealand).

Telecommunication revenues experienced a notable decline in 2009 but stabilised in 2010 and rebounded in 2011, the report notes.

But data services are growing at double‑digit rates in most OECD countries, and transport of data is now the major source of growth for network operators.

Few expect growth in traditional services such as telephony or text messaging, the report also says.

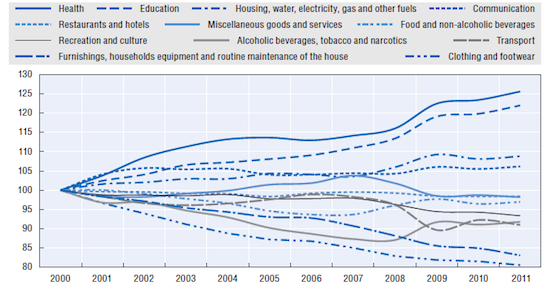

With 2000 as a baseline, typical consumer spending on communications is up about five percent to 2011.

No comments:

Post a Comment