These days, strategies are diverging. That might especially be true in developed markets, where actual practices have lead to more strategic diversity over the past couple of decades.

Those differences are driven, in large part, by a bifurcation of opportunity in the global telecommunications business, which is predicted by virtually all analysts to be growing, but unevenly.

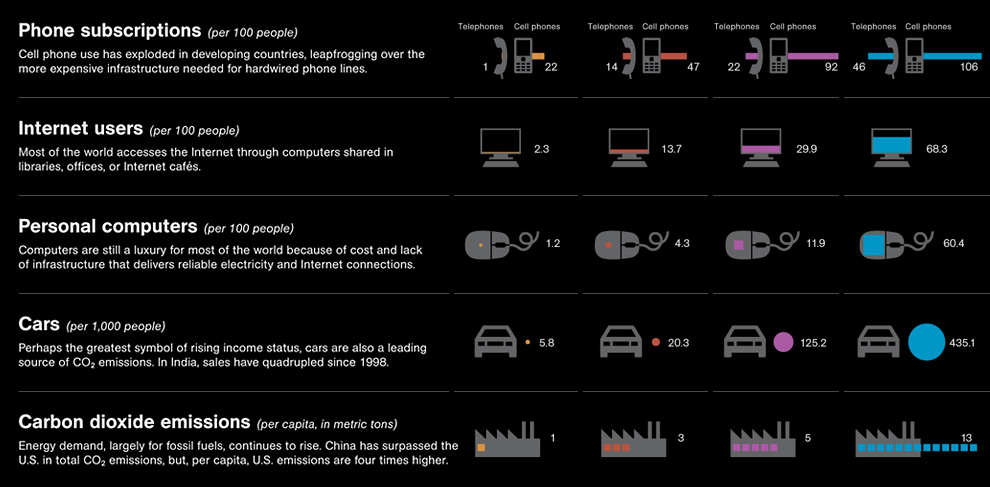

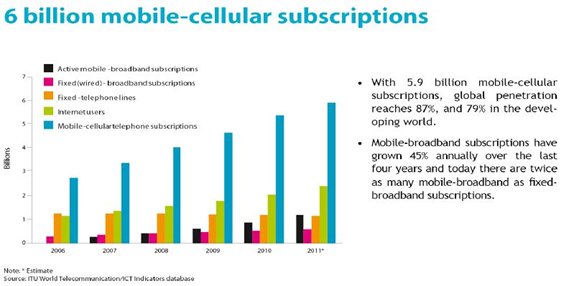

There are lots of places where phone penetration is 22 percent, for example, or where use of the Internet is about 23 percent, despite the fact that mobile penetration, in terms of “accounts,” now is as high as 79 percent, even in the “developing” countries.

Of course, usage even within a single country or region, and revenue prospects for service providers, are not distributed evenly. Generally speaking, growth opportunities are disproportionately found in the Asia-Pacific region, though Africa and Latin America are growth areas as well.

The obverse is true in much of of the developed world, where classic markets for voice and messaging are saturated, and even mobile broadband, the current growth driver, will face maturation not so long from now. That of course explains the serious and even furious pursuit of new growth drivers by executives in the mobile and fixed network service provider industries.

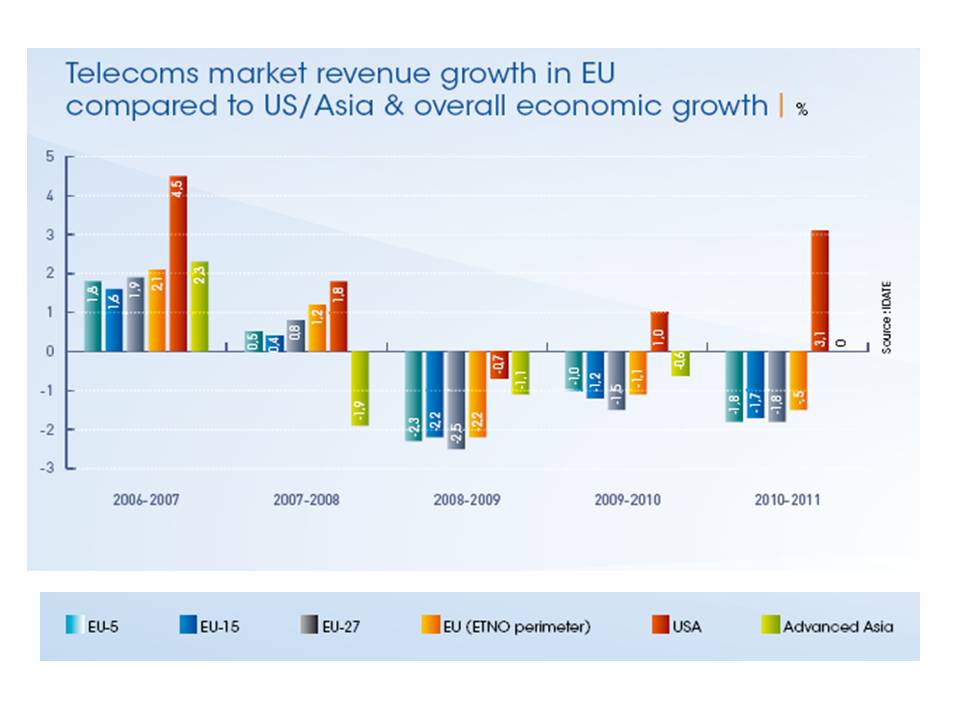

The European telecom service market decreased for the third year in a row, by 1.5 percent, the European Telecommunications Network Operators Association reports. You might blame a tough economy for the contraction, but ETNO points out that in the most-recent year, in a context of moderate economic recovery (+4.2 percent for current gross domestic product in the region), the lagging performance suggests structural changes, not just cyclical economic impact.

But some observers might argue that economic woes are having an impact.

The decline in fixed telephony revenues is accelerating (-8.3 percent in 2011 and –31 percent over the last five years), driven in part by a negative five percent growth of fixed lines in service. Since 2005, fixed line subscribership is down 22 percent. The bad news is that mobile revenues, long the driver of industry growth, also are declining (-0.6 percent)

Mobile voice revenues were down 4.7 percent in 2011 (–13.2 percent over the past three years), a decline driven by significant drops in some large countries: Spain (-8.3 percent),

France (-8.2 percent) and Germany (-7.1 percent).

Fixed network broadband revenue is the bright spot, as revenues were up 6.5 percent in 2011.

Mobile services, though, remain the bulk of telcos revenues, accounting for 52 percent of the total market (142.7 billion EUR in 2011).

The report also shows the divergence between European and the United States market, where it comes to revenue growth. Since 2006, U.S. service providers have done better than their European counterparts.

Precisely why that should be the case is not always so clear. One might argue that European markets are more competitive. One might argue European markets are more fragmented. One might argue that calling and texting tariffs have been higher, since there is more international roaming across Europe, compared to the continent-sized U.S. market.

Certainly, regulators have been squeezing revenue by mandating lower charges for cross-border roaming. Those lower tariffs of course will put pressure on gross revenue.

Moreover, Europe's share of the global telecoms market has been declining regularly over the recent years, from 31 percent in 2005 to just over 25 percent in 2011 as the gap between

global growth (+3.2 percent in 2011) and growth in Europe widens.

So different business strategies will make sense in different markets and parts of markets. Service providers in high-density markets with high per-capita income will be the first to find they must “outgrow” reliance on voice, messaging and even broadband access.

Service providers in low-density, high per-capita income areas will find they can rely on “basic” services for quite some time to come.

Service providers in high-density, low-income areas increasingly will be looking at ways to boost average revenue per user, while providers in low-density, low-income areas generally will be looking at ways to provide basic access services.

In telecom, there is no “one size fits all” strategy.

No comments:

Post a Comment